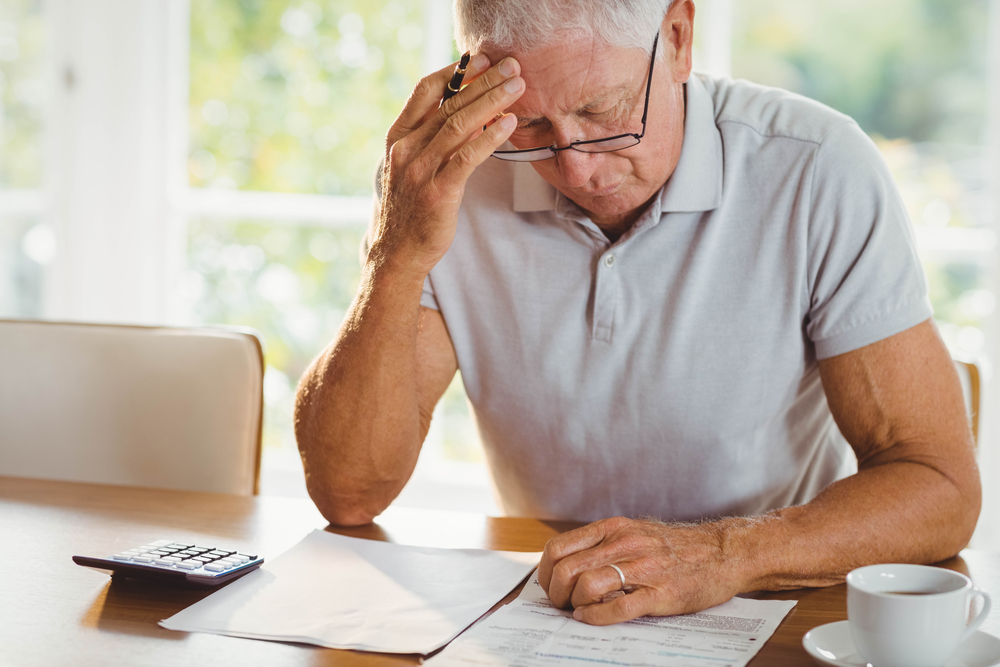

Although the inauguration is now in the rearview mirror, there is still much debate about which issues factored into people’s decisions at November’s ballot box. A recent survey of older adults echoes many election exit polls, however, finding that retirees are growing less optimistic about the economy and their personal finances than in prior years. How might these top retirement-related worries around money translate with regard to people’s senior living decisions?

Surveying older adults’ retirement risks and planning

The Society of Actuaries (SOA) Research Institute offers unbiased, data-driven research with the goal of identifying various societal challenges and then developing strategic solutions to tackle those issues.

Every two years since 2001, the SOA Research Institute has conducted an online Retirement Risk Survey of U.S. pre-retirees and retirees, aged 45 to 80, who represent a range of income levels. The survey’s objective is to gain a deeper understanding of this demographic’s retirement finance-related concerns and therefore devise ways to enhance older adults’ retirement planning strategies.

The most recent survey of 2,012 total older adult respondents, conducted in the spring of 2024, was the twelfth SOA-sponsored study focusing on people’s top retirement-related worries around their finances and retirement savings. The findings do not paint a rosy picture.

The complete results of the 2024 Retirement Risk Survey will be released in the coming months; you can view the full results of the 2021 survey here (PDF).

Worries about money and the unexpected

Overall, the poll results show that respondents feel worse off economically now as compared to those who took part in the 2021 survey. Older adults have become more aware of the need to financially prepare for unexpected events than those in earlier surveys. However, their retirement savings aren’t keeping up with inflation and/or expenses, which could impact their ability to afford their retirement years and, in particular, any long-term care needs.

Among the top retirement-related worries about money and savings uncovered by the most recent SOA Retirement Risk Survey:

Will my retirement income be enough?

Concerns about maintaining financial security in retirement are on the rise. A major issue is that savings and investments are failing to keep up with inflation. In fact, over three out of four pre-retirees (78%) and over half of retirees (58%) express this as one of their top retirement-related worries.

What about unexpected financial hits?

We’ve all had an unforeseen expense arise — perhaps the water heater breaks or the car needs a new fuel pump. But 20% of retirees and 35% of pre-retirees have faced a “financial shock” that resulted in a major monetary loss of more than 25% of their assets. Additionally, one in five pre-retirees have either run out of assets, had to downsize their home due to financial strain, or fallen victim to financial fraud.

>> Related: Crunch the Numbers: Aging at Home vs. Moving to a CCRC

How do I cope — emotionally and financially — with my caregiving responsibilities?

Reflecting the caregiving crisis in our country, many male and female pre-retirees (13%) are either currently providing care for or have at some point cared for someone other than their minor children. This might be an aging parent, adult children, or an extended family member. In comparison, 6% of male retirees and 9% of female retirees have had similar caregiving responsibilities.

As for the main impact of these caregiving responsibilities, 36% of male pre-retirees, a quarter of female pre-retirees (26%), as well as 35% of female retirees, reported “emotional or physical strain” as the top issue. Among male retirees, however, 14% highlighted long-term care planning as their top caregiving-related challenge.

What will I do if a loved one has a health crisis?

Fewer than 10% of retirees and pre-retirees provide significant financial support to family members, nor do they expect to receive financial help from loved ones. Additionally, more than a third of pre-retirees (38%) feel unprepared should a family member experience a medical emergency. Over a quarter of retirees (27%) share this concern.

>> Related: Pre-Crisis vs. Post-Crisis Planning: Confronting Life’s Unknowns

How can my retirement savings keep up with the rate of inflation?

Rising daily expenses are another top retirement-related worry, according to the survey. Over half of pre-retirees (51%) and more than a third of retirees (35%) report dealing with higher food and general costs. Also, 45% of pre-retirees and 29% of retirees say they are seeing increased utility bills. As a result, 44% of pre-retirees and 27% of retirees have had to make lifestyle adjustments.

The survey also highlighted older adults’ increasing concerns about sustaining long-term financial security in retirement. A major issue that emerged in the 2024 survey was the failure of retirement savings and investments to keep pace with the rate of inflation. In fact, 78% of pre-retirees and 58% of retirees cited this as one of their top retirement-related worries related to money. And as a result, more pre-retirees, especially those with annual incomes falling below $100,000, are adjusting their retirement savings strategies.

Are retirement planning technology tools safe to use?

The survey revealed that one of the most commonly used tools for retirement planning is actually online banking. Nearly two out of three survey respondents (62%) say they “often use” their financial institution’s online banking capabilities. However, many are hesitant to embrace other new automated retirement planning tools. Among their concerns are online security and the increasing risk of online fraud and scams.

Retirement-related worries around money weigh on senior living decisions

The results of this biannual SOA survey show that there are many issues weighing on the minds of America’s older adults with regard to retirement and their finances. And these concerns often play a significant role in shaping their senior living decisions.

For example, the fear of not having enough retirement income or savings to maintain their lifestyle or cover unexpected costs, like medical emergencies or long-term care, may lead them to seek what they perceive to be more affordable senior living options such as:

- Remaining in their current home

- Downsizing to a smaller home

- Relocating to an area with a lower cost of living

- Opting for a 55+ retirement community that has only independent living (versus a retirement community that offers on-site care services, such as a continuing care retirement community [CCRC])

>> Related: How CCRCs Can Ease Retirement-Related Fears

The monetary and unquantifiable costs of caregiving

Senior living decisions are often driven by a desire to reduce financial strain and live comfortably without draining one’s savings too quickly. However, the reality is that sometimes well-intentioned senior living choices, such as those listed above, can backfire.

For instance, remaining in the current home — or even downsizing to a smaller house — may seem like a cost-savings opportunity. However, any home will require interior and/or exterior upkeep, which can be costly and strenuous as you age.

And whether you opt to remain in your home or move to a 55+ independent living retirement community, there is the potential that you will require care. In fact, according to longtermcare.gov, “Someone turning age 65 today has almost a 70% chance of needing some type of long-term care services and supports in their remaining years.”

If you end up being among the 70% requiring care, the cost of paid in-home long-term care services can add up quickly. The Genworth Cost of Care Survey shows that in 2025, just 40 hours a week of in-home care services costs nearly $6,700 per month, on average.

Think you’ll save money and rely on unpaid care from a partner, adult child, or another loved one? There are still numerous costs associated with family caregiving. Some of those expenses are hard costs, like any necessary equipment or remodeling necessary to safely provide care. Other family caregiving costs can’t be quantified with a calculator. Instead, the costs come in the form of lost wages and benefits, emotional stress, and physical strain.

>> Related: The High Price of Family Caregiving

Hedging against the future’s unknown expenses

No matter your age, it is normal to feel anxious about the unknowns of the future. It is also common if your top retirement-related worries are around finances and whether you will have enough money to live comfortably and cover the costs of any care needs you may have down the road. But, there are ways to anticipate and prepare for the future’s unknowns.

As an example, some people may choose to invest in a long-term care insurance (LTCI) policy. Such policies can help cover the cost of long-term care, should you eventually require it. LTCI policies can be pricey, depending on your current age and health status, however. Many insurance experts suggest the ideal age for purchasing this type of coverage is in your mid-50s to early 60s.

The increasing prevalence of inflation and its effects on daily expenses may incentivize some older adults to downsize and seek out senior living options that include utilities, meals, and other services in one comprehensive package. This is a common pricing arrangement for many retirement communities, helping residents avoid the financial uncertainty of fluctuating housing costs.

Other older adults may decide to proactively move to a retirement community that offers on-site access to care, such as a CCRC (also called a life plan community). This choice can offer peace of mind to both the older adult and their loved ones, and in some cases, can ultimately result in cost savings.

CCRC pricing can vary depending on the location, amenities, and your contract type. Some also have an entry fee (which can reach into the six-figures). On the surface, a CCRC may seem to cost more than other types of 55+ communities. However, should you ever require care services, the decision to move to a CCRC can prove to be a wise investment, reducing stress on your and your loved ones while providing peace of mind, knowing you have a plan in place — and also possibly costing less, depending on the contract.